After quitting my big corporate job, I had an item on my checklist that I wasn’t sure how to tackle: rollover my 401k. Honestly, I didn’t care enough for it to make my to-do list. Why people rollover 401ks was lost on me. 7 months after I left the company my 401k was still invested, still growing. I still had access to it, and there were no penalties I’d encounter by leaving it where it was. So what was all the fuss about?

Eventually I had enough time on my hands to take a closer look.

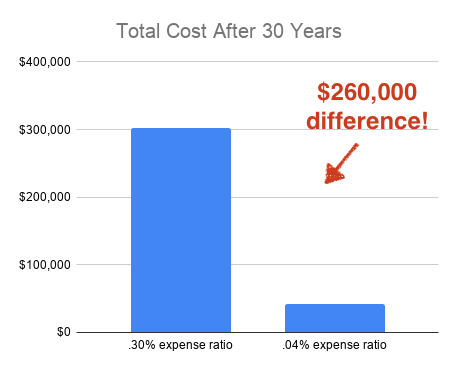

After some very basic research that took me about 15 minutes (20 if I count double-checking my math), rolling over my 401k to Vanguard would save me $260,000+ in fees over the next 30 years.

Holy cow!

Suddenly I cared very, very much.

Where are all these Fees coming from?

All $260,000 in fees came from one source: expense ratios. Expense ratios are the cost for the administration of the investment fund. Investment funds are those options you select when you first setup your account, such as the “Retirement 2050 fund.” Each investment fund has an expense ratio that’s charged annually as a percentage of the total amount in the fund. They are calculated with a simple equation:

Total investment amount * expense ratio = Annual fee

Let’s say for instance I had $10,000 in my 401k and the expense ratio is .45%. That means each year I pay a $45 fee to the broker. That doesn’t seem so bad, does it? But let’s remember that a retirement account like a 401k is intended to grow over time. And because you cannot withdraw until age 59.5, it’s an account that most people have for decades. For all of these reasons, that seemingly small annual fee is likely to become a very large amount.

Let’s take that same $10,000 401k and account for 10% average stock market growth over 30 years.

| Year | Investment Total | Interest Earned (estimated 10% interest rate) |

| 1 | $10,000.00 | $1,000.00 |

| 2 | $11,000.00 | $1,100.00 |

| 3 | $12,100.00 | $1,210.00 |

| 4 | $13,310.00 | $1,331.00 |

| 5 | $14,641.00 | $1,464.10 |

| 6 | $16,105.10 | $1,610.51 |

| 7 | $17,715.61 | $1,771.56 |

| 8 | $19,487.17 | $1,948.72 |

| 9 | $21,435.89 | $2,143.59 |

| 10 | $23,579.48 | $2,357.95 |

| 11 | $25,937.42 | $2,593.74 |

| 12 | $28,531.17 | $2,853.12 |

| 13 | $31,384.28 | $3,138.43 |

| 14 | $34,522.71 | $3,452.27 |

| 15 | $37,974.98 | $3,797.50 |

| 16 | $41,772.48 | $4,177.25 |

| 17 | $45,949.73 | $4,594.97 |

| 18 | $50,544.70 | $5,054.47 |

| 19 | $55,599.17 | $5,559.92 |

| 20 | $61,159.09 | $6,115.91 |

| 21 | $67,275.00 | $6,727.50 |

| 22 | $74,002.50 | $7,400.25 |

| 23 | $81,402.75 | $8,140.27 |

| 24 | $89,543.02 | $8,954.30 |

| 25 | $98,497.33 | $9,849.73 |

| 26 | $108,347.06 | $10,834.71 |

| 27 | $119,181.77 | $11,918.18 |

| 28 | $131,099.94 | $13,109.99 |

| 29 | $144,209.94 | $14,420.99 |

| 30 | $158,630.93 | $15,863.09 |

| $174,494.02 |

Incredibly, that $10,000 401k is estimated to be worth $174,494 after 30 years assuming a stock market average 10% return rate. This is due to the power of compound interest, and it is the reason why everyone emphasizes saving for retirement asap. The sooner you start saving, the more time you have for your savings to multiply in value.

Now let’s take that same 401k and account for the .45% expense ratio. We can do it using the same compound interest formula above, except we will use an interest rate of 9.55%. That’s the final rate if we take the 10% average return and subtract the expense ratio of .45%. Using a 9.55% interest rate, the same $10,000 401k is worth only $154,301.97 after 30 years, a difference of $20,192. That $20,192 is the amount paid in expense ratio fees.

The short version of this is:

401k total in 30 years at 10% interest rate: $174,494

401k total in 30 years at 10% interest rate – .45% expense ratio: $154,302

Total amount paid in expense ratio fees: $174,494 – $154,302 = $20,192

This person will pay a total of $20,192 in expense ratio fees over the course of 30 years on their $174,494 investment. Ouch! That’s a lot of money going to a fee!

Expense Ratio Cost Calculator

By now you’re up to your eyeballs in math that may not make sense to you. Don’t worry. You don’t have to know how to do these formulas on your own. You can use the expense ratio cost calculator below to find out how much expense ratios will cost over time. Just plug in the numbers and hit calculate for it to do all the compound interest formula for you.

By plugging my numbers into the calculator above I realized how much expense ratios were going to cost me in the long run. My 401k only had 18 funds that I could select from, and the average expense ratio was .30%. Meanwhile, my Roth IRA was invested in an S&P 500 index fund with an expense ratio of only .04%. That is 7 times less than my 401k funds!

After finding my expense ratios, I plugged them into the expense ratio cost calculator to see how much each would cost me over time. This is where I learned that the expense ratios of my old 401k funds were going to cost $260,000 more than my Vanguard fund over the course of 30 years. I don’t know about you, but finding out I could save $260,000 in fees was highly motivating.

It literally pays to find out how much you’re paying in expense ratios and look into a 401k rollover.

How Do You Find Your Expense Ratios?

There are lots of companies that sponsor 401ks (Merrill Lynch, Fidelity, TD Ameritrade, Charles Schwab, etc.), and the steps to find the expense ratio are different for each of them. Generally you can find it by signing into your account online, and find the fund(s) you’ve selected. Once you find the fund, you will see the expense ratio in the details of the fund.

Account -> Fund -> Expense Ratio

It took me about 15 minutes to find the funds and corresponding expense ratios in two different accounts. Remember that the 15 minutes it took to find the expense ratios, then plug them into the calculator above is how I found out I could save 6 figures in fees.

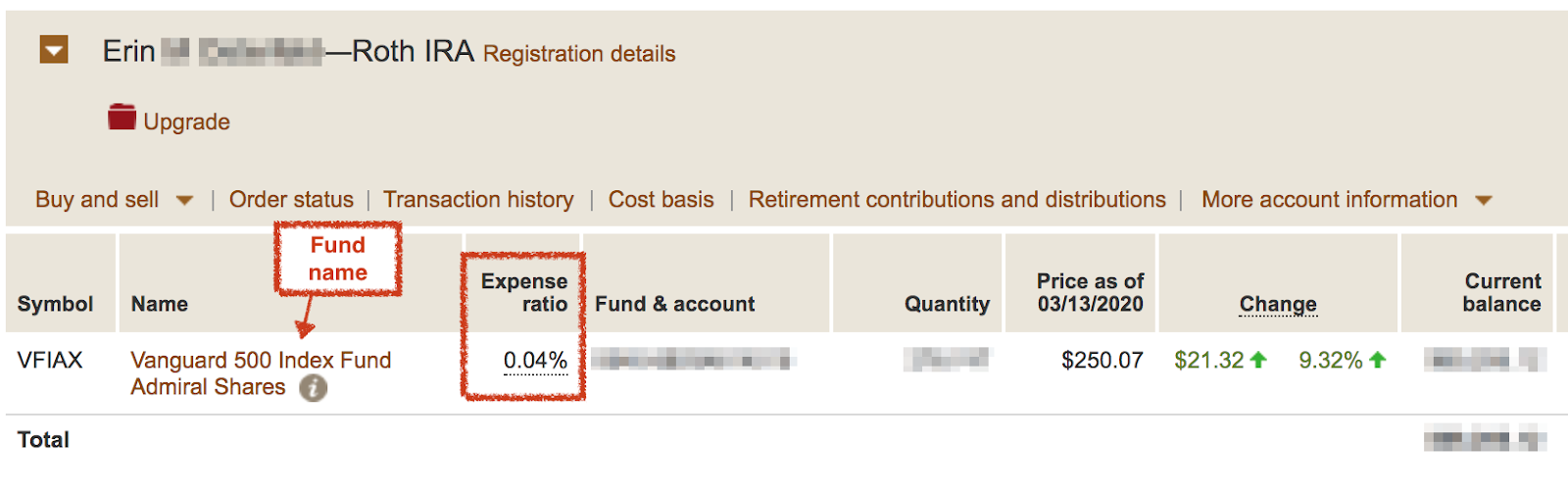

Here’s where I found the expense ratios within my Roth IRA at Vanguard and my 401k at Merrill Lynch. Keep in mind that the funds in my account may be different than yours.

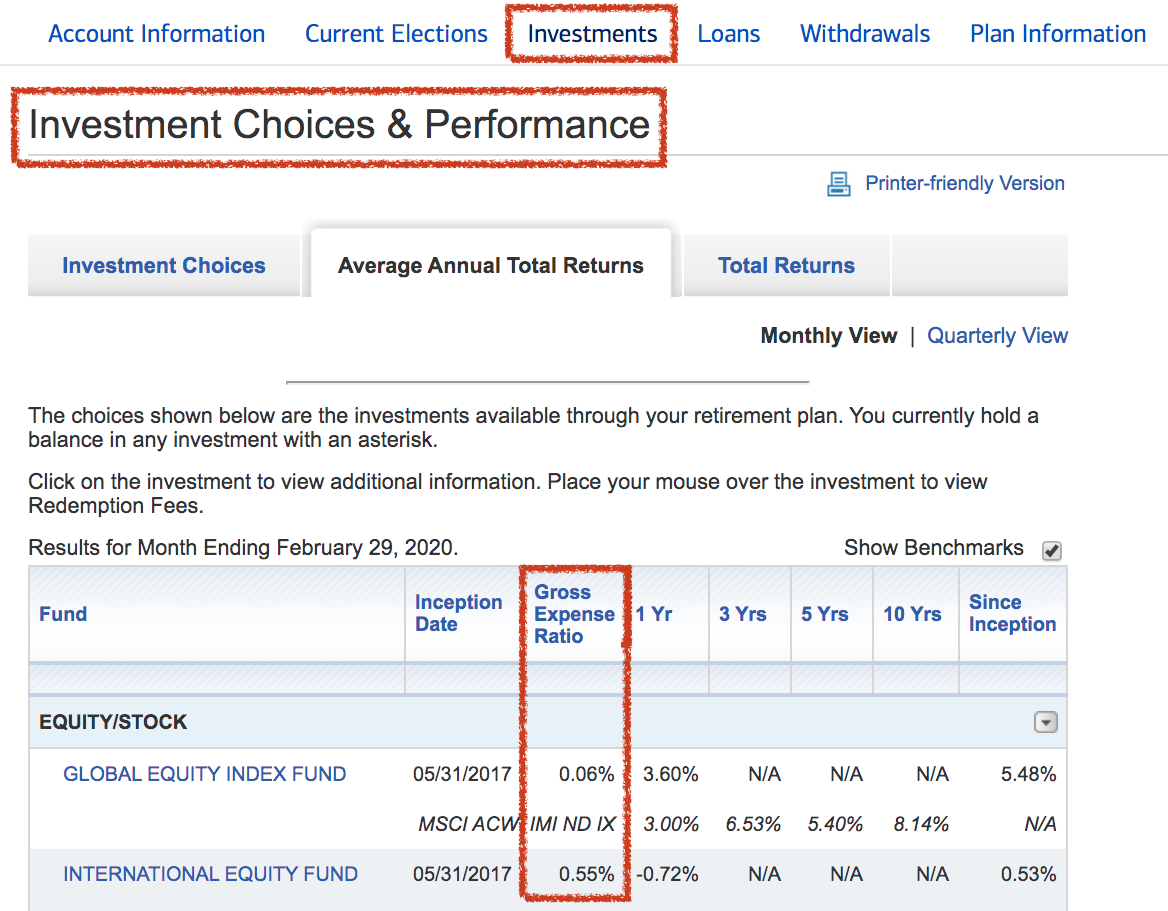

Merrill Lynch was a little more complicated. After signing in and selecting my 401k plan, I had to find the “Average annual total returns” tab under “Investment Choices and Selection.”

Now What?

So you found the expense ratios. If you like the fund(s) and their expense ratios, there is no need to do anything. You’ve been spending a reasonable amount on fees for the duration of your 401k. That’s great!

If you are unhappy with your fund performance and/or the fees associated with them, you can either change funds within the 401k or rollover the 401k for more options.

Most importantly, find the fund you want to invest in. As an average investor at best, I like to pick index funds. They are a collection of many companies stock, so they work for those of us who like to “set it and forget it.” Index funds also generally have low fees. If you don’t know what fund to select, consider talking with your financial advisor or someone you trust with financial decisions.

After selecting a fund, decide which investment company you want to work with. If your existing investment company offers the fund you want, there is no need to change. Since mine did not, I chose to rollover my 401k to Vanguard because I already had a Roth IRA and a personal investment fund with them. Choosing Vanguard gave me the opportunity to consolidate accounts while also reducing fees. Finally, I could have all of my retirement accounts in a single place.

How to Rollover a 401k to Vanguard

About 5 seconds after I saw how much I would save by rolling over my 401k to Vanguard, I got to work. I called Vanguard at 888-499-970 to initiate the transfer. Although they offer instructions on how to do this online, it can be easy to make a mistake that can cost thousands. I wanted to have a professional direct the transfer so that it was done correctly.

I could have called Merrill Lynch for assistance transferring my 401k, but I find the company receiving my business tends to be easier to work with than the company I’m leaving.

The representative from Vanguard had clearly been through this before. She was friendly, precise and professional. We bridged Merrill Lynch into the call, and within 20 minutes had the transfer underway. All I had to do was verify my identity by providing my SSN, employer start date, and employer termination date to Merrill Lynch to validate my account and begin the asset transfer. From there I gave permission to the Vanguard representative to handle the rest. Easy peasy.

8 days after our call the funds were deposited into my Vanguard account. All of this cost me about 45 minutes and a $26 account termination fee from Merrill Lynch. For a savings of over $260,000, the time and money were well worth it!